The Case of the Disappearing Greenhouse Gas Emissions

- Date: 16 February 2023

- Author: Katherine Devine and Emily Moberg, WWF Markets Institute

The news is full of headlines about companies making commitments to reduce their greenhouse gas (GHG) emissions. Given the alarming pace of climate change and governments’ failure to slow it, companies’ contributions are vital to both the planet and their bottom lines. Companies have a stake in mitigation efforts as climate change presents a real risk to their operations and infrastructure. However, behind all of the ambitious goalsetting and initial progress lies a secret that’s ripe for exploitation: product-level GHG accounting is so fragmented and flexible that it’s incredibly difficult to hold companies and sectors accountable for emissions reductions. What’s more, because companies can choose which methodologies to use and companies in adjacent industries may choose different methodologies (think: beef and leather), some emissions are simply not being accounted for once we get to the end products.

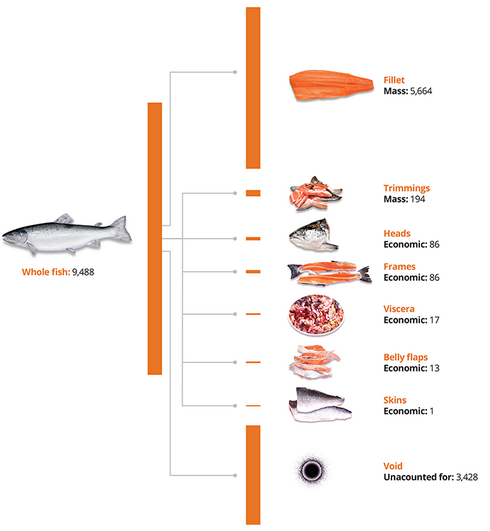

Take this figure, which represents the various products resulting from one salmon. More than a third of emissions are “lost” due to some allocations occurring by mass, and others by economic value (see “Greenhouse Gas Accounting Efforts Undermined by Disparate Tools & Frameworks” for more detail on allocation methodology differences). This issue isn’t unique to salmon; it’s a challenge across the board.

Illustration showing GHG emissions in thousand tons CO2e to produce live salmon and how those emissions are allocated after slaughter if each buyer uses the allocation method that minimizes their footprint. When this occurs, about 1/3 of total emissions are unaccounted for.

Credit: Xenia Zhao

…

This is also a difficult problem to solve – varying methodologies have cropped up not only for convenience, but also because measuring GHG emissions in agriculture is complex; the emissions from livestock like cattle are very different from row crops like corn. There is also huge variability in the GHG emissions for producing the same product; emissions for the same crop or livestock product can vary 10 to 100-fold depending on production practices, climate, and other factors, like whether natural habitat was converted for cropland.

To change this, we need to speak the same language on climate change impacts – whether this is through globally standardized methodologies and reporting requirements or through clear frameworks that allow translation and comparison across methodologies. GHG accounting standards provide guidance on what and how to measure these emissions. There are many GHG accounting standards with different purposes; some are intended to compare a company’s performance over time while others are focused on comparing across a single product. Many of these standards offer flexibility so they can be effectively applied to very different industries.

However, if the emissions arising from a single source are measured two different ways, the estimates will be different. Without overarching regulation, companies can cherry-pick methodologies to produce a more favorable outcome. This presents a challenge: how can buyers distinguish whether a lower GHG footprint from a purchased product reflects real improvements or methodological differences? How can investors or state actors identify leaders from laggards? And how can we stop “losing” the disappearing emissions across supply chains? Because while the numbers may look better for individual companies, the emissions are still occurring whether they’re appropriately accounted for or not.

This issue is exacerbated across supply-chains, where each actor’s accounting methods influence the Scope 3 emissions total for their buyers and suppliers. When accounting methods aren’t harmonized, there is large risk that significant emissions may be unclaimed as they travel downstream, such as with the previous salmon example.

To address this, companies can take action internally by requesting and providing information on GHG accounting methods to suppliers and buyers. Many companies share suppliers or portions of their supply chains. By collaborating on standardizing information requests from suppliers, individual quality control of data and information harmonization can occur more quickly. Many sectoral groups, such as the Global Salmon Initiative, are working on this harmonization.

At the same time, companies cannot wait before taking climate action. A 1.5°C future requires significant emissions reductions every year. It is thus vital that companies ramp up emissions mitigation efforts in their own operations and in their supply chains while simultaneously collaborating on improving GHG accounting methods. Both harmonized measurement and ambitious mitigation action are urgently needed to make progress against climate change, and to understand that progress consistently and accurately. After all, emissions don’t actually disappear even when they don’t show up on a company’s emissions balance sheet.

Read the full analysis: Greenhouse Gas Accounting Efforts Undermined by Disparate Tools & Frameworks

About the authors:

Katherine Devine, Director, Business Case Development, WWF Markets Institute

Katherine brings more than 15 years of experience working at the intersection of business and conservation. Collaborating with internal and external experts, she crafts concise, digestible business cases on a range of topics related to food production, analyzing how sustainability can lead to positive bottom-line impacts and reduced risk.

Emily Moberg, Director, Scope 3 Carbon Measurement and Mitigation, WWF Markets Institute

Emily uses her quantitative research and modeling background to identify the cutting-edge trends and solutions around climate mitigation in agriculture and aquaculture. At WWF, her work has included research on greenhouse gas impacts of commodities ranging from coffee to tuna to beef, and strategic efforts to choose appropriate measurement and accounting tools with industry groups.